All Categories

Featured

Table of Contents

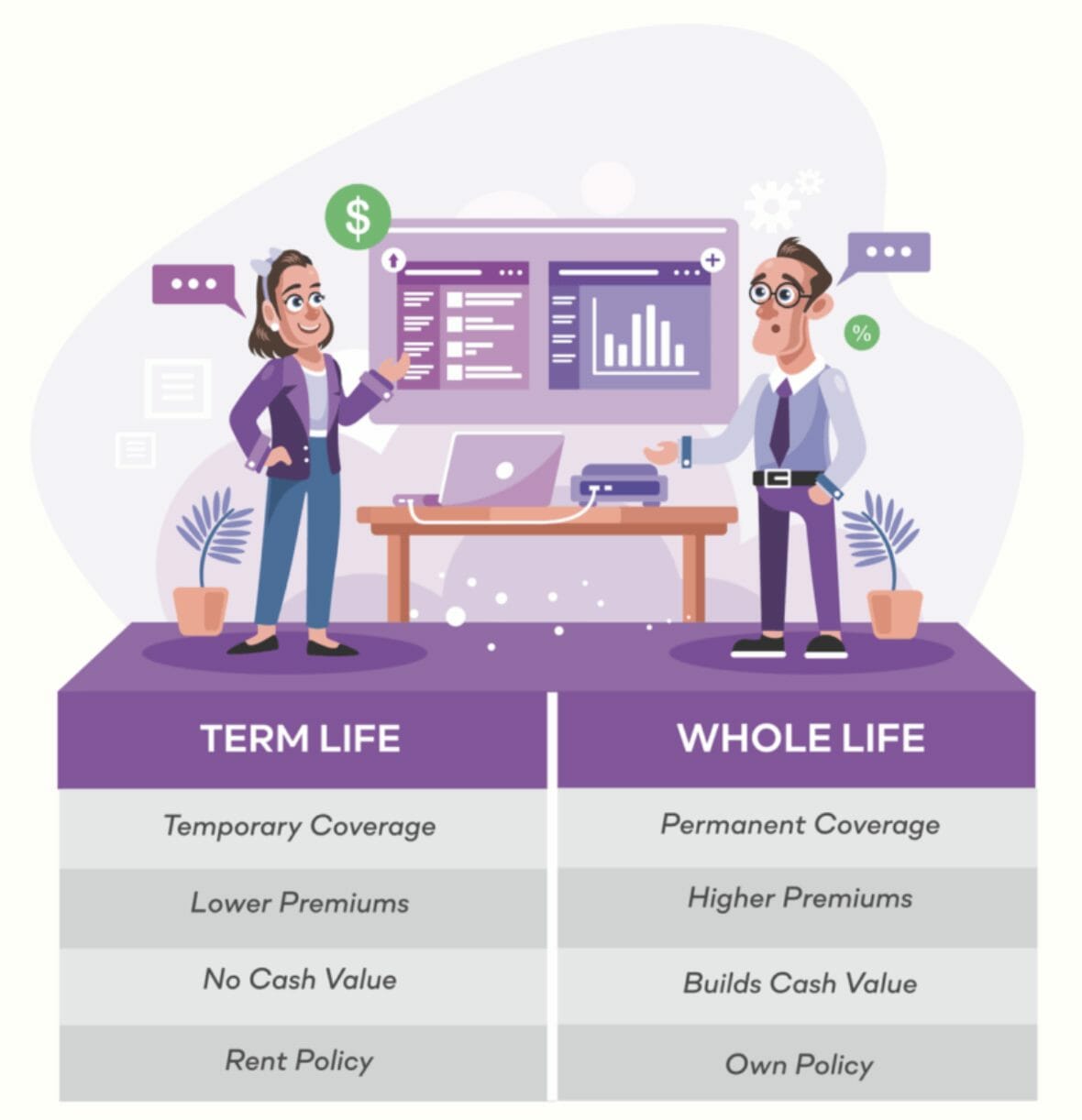

The are whole life insurance and universal life insurance. The cash money worth is not included to the fatality benefit.

After ten years, the money worth has expanded to around $150,000. He secures a tax-free lending of $50,000 to begin a service with his brother. The plan financing rate of interest rate is 6%. He repays the loan over the next 5 years. Going this route, the rate of interest he pays goes back into his policy's money value instead of a financial organization.

How To Start Infinite Banking

The concept of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a money specialist and fan of the Austrian college of business economics, which advocates that the worth of products aren't explicitly the result of conventional financial structures like supply and demand. Rather, individuals value money and items differently based upon their economic status and requirements.

One of the challenges of typical banking, according to Nash, was high-interest rates on fundings. Long as financial institutions set the passion prices and lending terms, people didn't have control over their own wide range.

Infinite Financial needs you to possess your financial future. For goal-oriented individuals, it can be the most effective financial tool ever. Right here are the benefits of Infinite Financial: Probably the solitary most valuable facet of Infinite Banking is that it enhances your capital. You do not need to go with the hoops of a standard bank to obtain a car loan; just request a policy funding from your life insurance policy firm and funds will be offered to you.

Dividend-paying whole life insurance policy is really reduced danger and supplies you, the insurance policy holder, an excellent offer of control. The control that Infinite Banking provides can best be organized right into two groups: tax obligation advantages and possession securities.

Infinite Banking Concept Review

When you utilize whole life insurance policy for Infinite Banking, you participate in an exclusive agreement between you and your insurance provider. This personal privacy provides specific possession securities not found in other financial automobiles. These securities might vary from state to state, they can consist of protection from asset searches and seizures, security from judgements and security from financial institutions.

Whole life insurance plans are non-correlated assets. This is why they function so well as the monetary foundation of Infinite Financial. No matter of what takes place on the market (stock, realty, or otherwise), your insurance coverage retains its worth. A lot of people are missing out on this necessary volatility buffer that aids secure and grow wealth, instead dividing their cash right into 2 pails: checking account and investments.

Whole life insurance is that 3rd bucket. Not just is the rate of return on your entire life insurance coverage plan ensured, your fatality advantage and premiums are likewise guaranteed.

This framework aligns flawlessly with the concepts of the Perpetual Wide Range Technique. Infinite Financial interest those looking for higher financial control. Here are its major benefits: Liquidity and availability: Plan lendings give immediate accessibility to funds without the restrictions of traditional small business loan. Tax obligation efficiency: The cash money worth expands tax-deferred, and plan financings are tax-free, making it a tax-efficient device for building wide range.

Bank On Yourself Life Insurance

Asset security: In many states, the money worth of life insurance policy is shielded from lenders, adding an additional layer of monetary safety and security. While Infinite Banking has its advantages, it isn't a one-size-fits-all remedy, and it comes with substantial drawbacks. Below's why it might not be the very best approach: Infinite Financial typically calls for elaborate plan structuring, which can confuse insurance policy holders.

Think of never needing to stress over small business loan or high rates of interest once again. Suppose you could borrow cash on your terms and build wealth concurrently? That's the power of limitless financial life insurance policy. By leveraging the cash value of entire life insurance policy IUL policies, you can grow your wide range and borrow cash without depending on standard financial institutions.

There's no set financing term, and you have the flexibility to choose on the settlement timetable, which can be as leisurely as settling the loan at the time of death. This versatility reaches the maintenance of the lendings, where you can go with interest-only settlements, keeping the funding balance level and manageable.

Holding cash in an IUL fixed account being attributed rate of interest can usually be better than holding the money on deposit at a bank.: You've always imagined opening your very own pastry shop. You can obtain from your IUL plan to cover the preliminary costs of renting out a room, buying devices, and employing team.

Cash Flow Banking Insurance

Individual car loans can be acquired from conventional banks and credit report unions. Obtaining money on a credit history card is typically really pricey with annual percent prices of interest (APR) typically getting to 20% to 30% or even more a year.

The tax obligation treatment of policy car loans can vary substantially relying on your country of house and the particular regards to your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy finances are typically tax-free, supplying a significant benefit. Nonetheless, in other jurisdictions, there might be tax effects to think about, such as potential taxes on the loan.

Term life insurance only supplies a fatality benefit, without any type of money value buildup. This means there's no cash worth to borrow versus.

For car loan officers, the extensive regulations enforced by the CFPB can be seen as cumbersome and limiting. Financing officers typically argue that the CFPB's policies develop unnecessary red tape, leading to more documentation and slower funding processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) guideline and the Ability-to-Repay (ATR) demands, while targeted at securing customers, can lead to delays in shutting offers and enhanced operational costs.

{kind=link}

Table of Contents

Latest Posts

Infinite Financial Systems

Nelson Nash Net Worth

Infinite Banking Concept Videos

More

Latest Posts

Infinite Financial Systems

Nelson Nash Net Worth

Infinite Banking Concept Videos